Navigating the Mortgage Maze: A Guide for New Doctors

Essential tips for new doctors on securing a mortgage after residency.

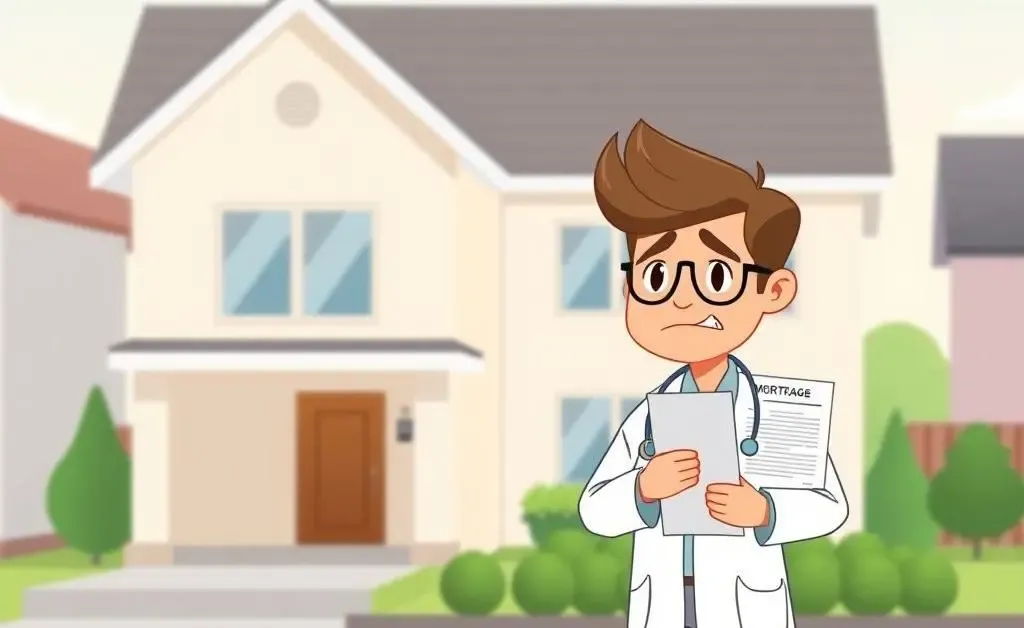

So, you’ve made it through medical school, survived residency, and now you’re gearing up for your first full-time role as a doctor. Congratulations on getting here! But wait—now you’re thinking about buying a home, and the world of mortgages seems as tangled as a set of ECG cables. Fear not; I’m here to help unravel some of that confusion.

The Backstory: Balancing Finances and Home Dreams

Let’s step into the shoes of Dr. Jamie—a fictional graduate transitioning from residency to full-time practice. Jamie has worked hard, juggled 24-hour shifts, and occasionally slept sitting up (though not recommended). With their residency wrapping up, Jamie is looking forward to more stable hours—and stable roots with a new home.

Why a Mortgage Now?

Many new doctors, like Jamie, wonder why they should dive into home buying shortly after residency. The reasons to consider this include:

- Stable income prospects

- Building equity instead of renting

- Taking advantage of lower interest rates

It’s understandable to be both eager and cautious. Mortgages can feel intimidating, but with the right guidance and tools, new doctors can make wise decisions.

Steps to Securing a Mortgage

The first task for any new doctor is to assess your financial situation. What debts do you have? How steady is your income? Once you have those answers, you can look at these practical steps:

1. Check Your Credit Score

Your credit score will greatly influence your mortgage terms. A higher score can secure you lower rates, which means smaller monthly payments—ideal for someone just starting out in their practice.

2. Determine How Much Home You Can Afford

Create a realistic budget including all potential expenses alongside your anticipated new salary. Consider talking to a financial advisor if numbers aren't your thing. This budget will be your compass.

3. Get Pre-Approved

A mortgage pre-approval gives you an edge when it’s time to make an offer on a home. It shows sellers that you mean business. Plus, it helps set a firm limit on your budget to keep you grounded.

Understanding Loan Options

There are several loan types available, each with their quirks. Fixed-rate loans offer predictable payments, while adjustable-rate mortgages might start lower but fluctuate. Another option is a doctor loan, specifically designed for medical professionals with benefits like no PMI (Private Mortgage Insurance) despite low down payments.

Ask for Help!

This might sound simple, but don’t hesitate to consult trusted colleagues or family who have been through the process. Learning from others' mistakes and triumphs can save time and stress.

Wrapping Up

There you go, a roadmap to navigate the mortgage maze as a new doctor. With patience and the right information, you'll be able to plant roots confidently. And if you have any other tips or questions, I’d love to chat. What’s your biggest concern about entering the world of homeownership?