Switching to a Cash Management Account: Benefits and Considerations

Discover how a cash management account can be your new primary checking solution.

Have you ever found yourself overwhelmed by monthly fees or disappointed by the meager interest rates of your primary checking account? If so, switching to a cash management account (CMA) could be just the change you need to make your personal finance journey smoother.

What is a Cash Management Account?

Simply put, a cash management account is a hybrid between a checking and a savings account offered by investment firms and fintech companies. It usually offers higher interest rates and often comes with minimal to no fees.

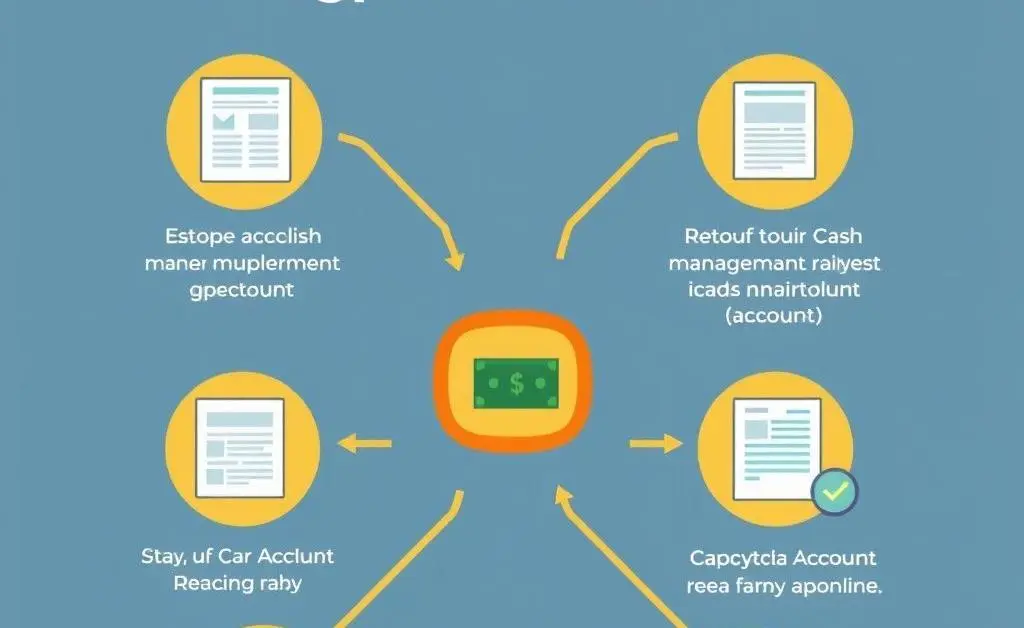

Benefits of Switching to a CMA

Here's why a CMA might be your best option:

- Higher Interest Rates: Unlike traditional checking accounts, CMAs often provide interest rates more comparable to savings accounts.

- Lower Fees: Many CMAs have no monthly fees, ATM surcharge reimbursements, and no minimum balance requirements.

- Ease of Access: Get the benefits of ATM networks, debit card access, and even check-writing capabilities.

Key Considerations

While there are many perks, it's essential to consider a few potential downsides:

- Investment Account Requirements: Some CMAs might require you to open an investment account with the provider.

- FDIC Insurance: Check if your CMA is insured by the FDIC, providing security similar to checking accounts at a bank.

- Features: Ensure the account has all the banking features you need—and some don't match the convenience of physical banks.

How to Set Up a CMA

Transitioning to a CMA is easier than you might think. Here's a simple guide:

- Research CMA providers to find a perfect fit based on fees and features.

- Check for FDIC insurance as a security measure.

- Complete the application process, often entirely online.

- Transfer your funds and enjoy your new checking solution.

Is It Right for You?

Choosing whether to switch to a cash management account depends entirely on your financial goals. Comparing the pros and cons, ask yourself if the potential savings and conveniences align with what you value most in a banking account.

What are your thoughts on using a CMA as your primary checking? Let’s dive into this topic and explore how you can optimize your finances for a brighter future!